Claims were recently made by a Twitter user that the computer algorithm which determines the credit limit for the new Apple Card is biased, causing someone to receive a much lower credit limit than her husband, despite being married and sharing an income. These posts have gone viral and have now been picked up by news media. The goal of this article is to explain how the credit underwriting process typically works and offer some possible explanations for the difference in credit limits. My hope is that users will take this information into account before jumping to conclusions of gender bias.

First, a disclaimer. The information presented in this article is based on general credit decisioning information collected from bank underwriting departments, credit managers and loan officers. For the sake of brevity, we have simplified many of the concepts, so please understand that when we say factor A is not used in a decision, it means that the factor is not primarily or largely used in a significant way that would likely affect the outcome. All lending institutions are different, use different scoring models from different vendors, use unique methods to analyze credit profiles and neither us nor anyone else can say exactly what goes into the decision-making process. We can only give you general information about how the lending industry traditionally assesses credit and determines approval and terms.

So what’s the issue?

On November 7, a Twitter user posted a tweet that indicated the following points:

- He and his wife file joint tax returns.

- He and his wife live in a community property state.

- He and his wife have been married for a long time.

- He received 20 times the credit limit his wife received when applying for the Apple Card.

Let’s address each point specifically:

- Banks don’t have visibility into or use tax returns or income reported to the IRS in credit decisions.

- Banks don’t have visibility into or use your state’s property and marriage laws as a factor in credit decisions.

- Banks don’t use length of marriage as a factor in credit decisions.

- There are two possible explanations outlined in this article that may account for this.

In a later post, the user added that he and his wife have comparable credit scores.

How are credit limits determined?

Let’s look at some of the factors that banks use in granting credit decisions and determining credit limits.

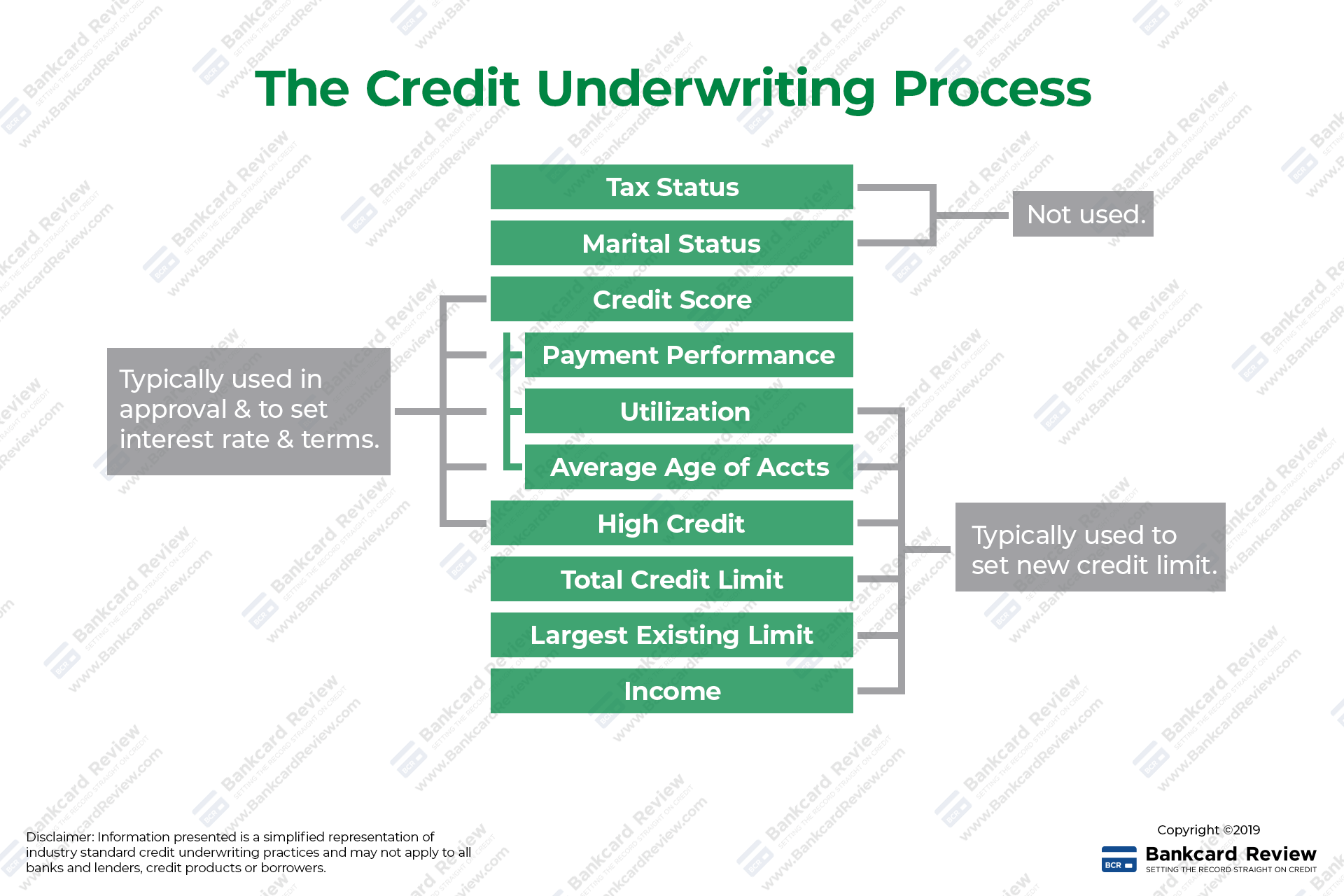

First, it’s important to understand what comprises a credit score. A credit score is based on your credit performance and primarily made up of the following three components in rough order of importance:

- Timeliness of payments - Are all your payments made on time, and are there any late payments, and how late?

- Utilization - What percentage of your total available credit is used and how much is available?

- Average age of accounts - What is the average age of all your revolving accounts?

Here are some factors that DO NOT figure into your credit score, and the reason.

- High credit - Your high credit amount is the highest amount of money you’ve borrowed and successfully made payments on. This is an indicator of your credit capacity, since having successfully managed a high dollar amount of credit will give banks confidence in your ability to manage larger amounts. This does not and cannot factor into your credit score because it will vary across geographical and demographical groups, as well as fluctuate with inflation, consumer borrowing habits and other factors. If this were to be included in your score, it would have to be indexed to some average amount which would place higher income individuals with larger income and credit usage at a significant advantage and lower income people at a significant disadvantage.

- Total credit limit - Your total credit limit is the total of all revolving credit limits on your report. For example, if you have a store card with a $500 limit and a Visa card with a $2000 limit, your total credit limit will be ($500 + $2000) = $2500. This is important to show how successful your existing banking and credit relationships are, and a higher number gives banks confidence in your ability to continue to handle large amounts of credit. However, too much available credit can also cause you to be declined or given a lower limit, as banks start getting nervous when a consumer has too much unused credit.

Since the above numbers (high credit and total credit limit) don’t factor into your credit score, banks typically assign a low weight to your score when determining your new credit limit. Here’s a quick and dirty infographic listing the various factors mentioned and where they are used in the underwriting process.

What we can see here is that the major factors influencing your new credit limit are your high credit, total credit limit and largest existing credit limit. In fact, I have been through manual underwriting processes for credit cards where the underwriter made it clear that the bank bases your new credit limit primarily on existing limits with previous issuers. Here’s how the process typically works:

- The underwriter (or system) determines whether you are approved or not based on your score, and some other data points which may preclude your approval (such as bankruptcy or collections). There is normally a minimum cutoff score which is rarely disclosed.

- Your interest rate is then is determined based primarily on your score and possibly some other minor factors. This is normally tier-based.

- Your credit limit is then assigned based on your income, high credit, largest existing limit, total credit, utilization and some other minor factors.

As you can see, your score plays very little into your credit limit determination. By the time the bank underwriter (or algorithm) is setting your credit limit, it’s looking more at income, high credit, existing limits and other dollar amount related factors.

Back to the Apple Card issue

It's entirely possible, and in fact likely, that she received a smaller credit limit due to factors other than her score.

There is one other possibility which may account for the difference in credit limit. Many new credit algorithms are taking a modern approach to underwriting by examining additional data not traditionally used in lending decisions, such as career type, education, accomplishments, social factors and other various factors. (See Upstart.) If this is the case, it may provide an explanation as to why a prominent and visible tech founder and the founder of one of the world’s largest companies were granted a larger than average credit limit while their spouse was granted an average credit limit similar to what anyone else with a similar profile would have been.

Of course, none of us know the specific reasons for the difference in credit limit, and probably never will, since neither Apple nor Goldman Sachs are likely to release a statement that would disclose very personal and private information or give away too much information about their internal process. One thing we do know for sure, is that we should avoid jumping to conclusions of gender bias without examining the exact same data the bank used in making the decision, and at least making an attempt to understand why the outcome is what it is.